景気のサイクルについて

前日の記事(Ray Dalioの投資哲学と手法)にあった債務のサイクルと類似のinvesmtnt clockについて解説.

The "Investment Clock" 投資のサイクル

✓ 概念自体はMerrill Lynchにより提示された。

Phase 1 - Reflation phase:低成長&低インフレ - Bear market

供給過多かつ需要小 →commodity prices low (down inflation)

FEDは金利を低下させる → Bond is the best

Phase 2 - Recovery phase:高成長&低インフレ - goldilocks phase

FEDの金融政策(QEなど)が功を奏する → Stock is best.

Phase 3 - Overheat phase:高成長&高インフレ

生産性が低下することでインフレが上昇。

Volatility returns as bond yeilds rise and stocks compete with higher yeilds for capital flows. → Commodities are best

Phase 4 - Stagflation phase:低成長&高インフレ

FEDは金利を上げ続ける。(失業率が上昇するまで続く) → Cash is the best.

Preferable asset allocation for each relative phase from Merrill Lynch

1. Cyclicality: 成長が加速する際は、Stock & Commodities do well. (Tech & Steel).

成長が減速するときは、Bonds, Cash, and defensive outperform.

2. Duration: インフレが低下する際は、.financial assets do well. Growth stockもOK.

インフレが上昇する際は、Commodities and Cash do best. Value stocks outperform.

3. Interest rate-sensitives:Banks and consumer discretionary stocks が金利に敏感, reflation and recovery時に良い結果

4. Asset Plays: Insurance stocks and Investment Banks are often bond or equity price sensitive, doing well in the Reflation or Recovery phases. Mining stocks are metal price-sensitive, doing well during an Overheat.

今はサイクルのどこにいるのか? (2017-2018年)

1. GDP gap

Difference between the economy's actual GDP and its potential (when producing at full capacity).

Zero line = full economic capacity.

GDP gapが正の時、生産過剰。→インフレが上昇し、FEDは金利を上げる。

This means we're in the later phases of the cycle but not at the end.

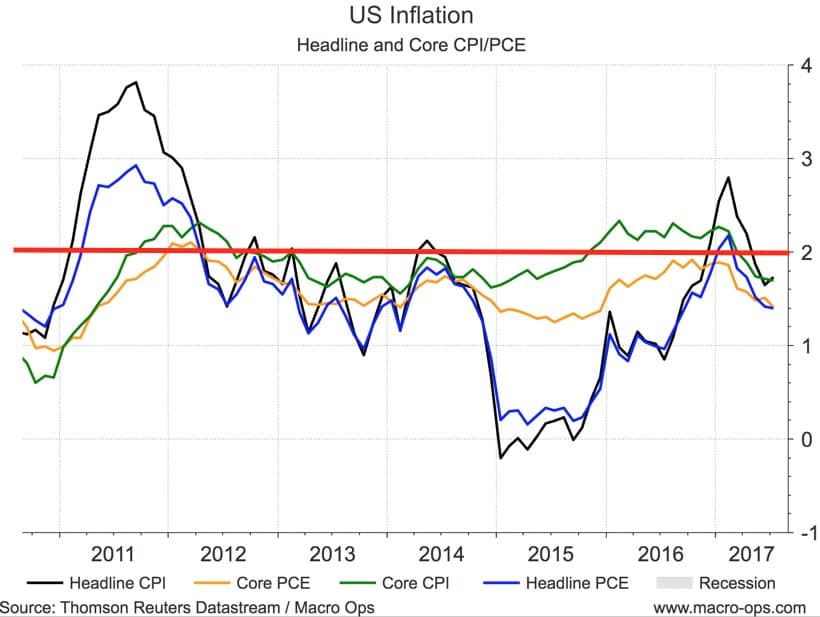

2. Inflation.

この先、インフレがどう変化するかを推測するのは困難。

一般に、インフレは、ドルや賃金に依存する。

cf. ドル安→コモディティ高(インフレ)

Commodities投資のススメ

1. 経済が過熱した状態ではcommoditiesがbest perform

2. Commoditiesはstockに比べて2000年以来最安値。(下図)

Bottom line

Commoditiy Index total return ETN (DJP)